The Securities and Exchange Board of India (“SEBI”) held its Board Meeting on September 12, 2025, approving proposed amendments to various regulations as elaborated below.

(i) Amendments to Securities Contracts (Regulation) Rules, 1957 relating to minimum public offer and timelines to comply with minimum public shareholding for issuers with the objective to enhance ease of doing business

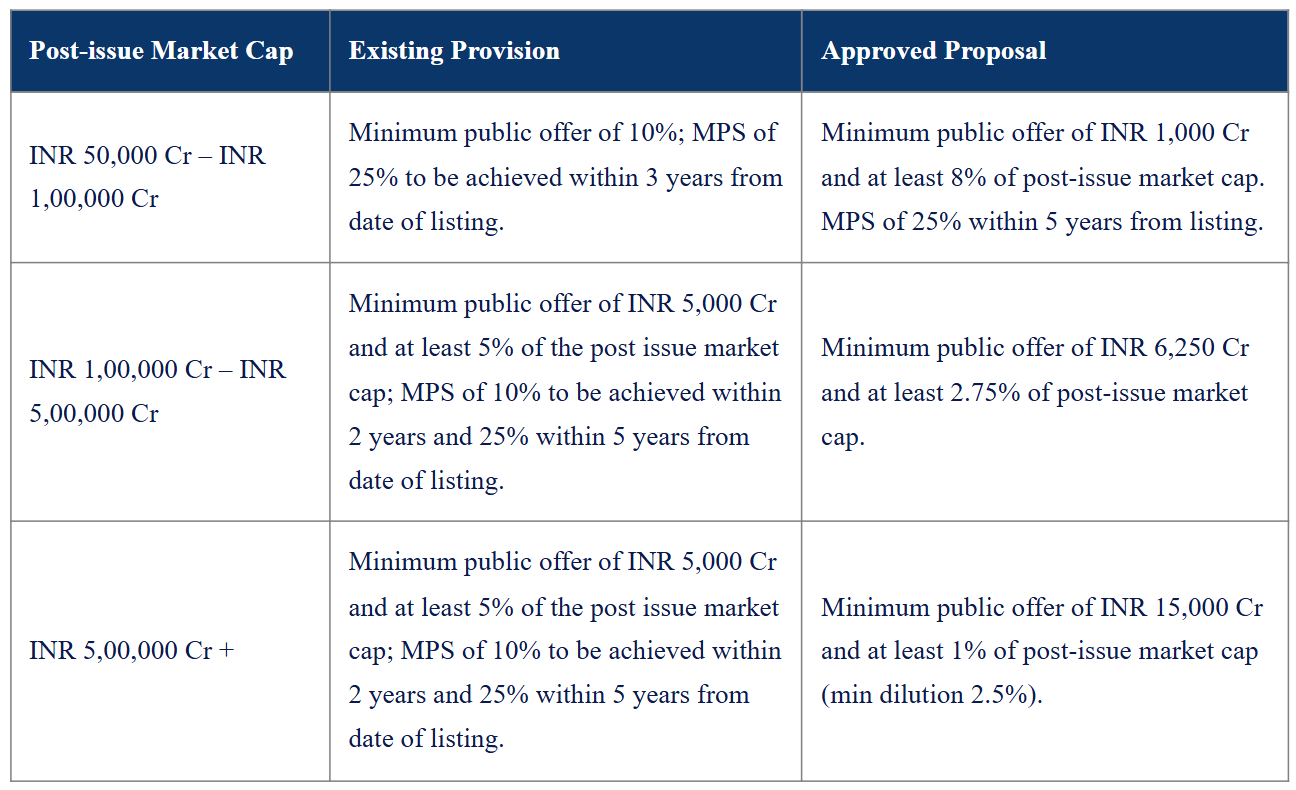

SEBI has decided to recommend to the Ministry of Finance the following changes in the Securities Contracts (Regulation) Rules, 1957 (“SCRR”) to revise the Minimum Public Offer requirements and timelines for achieving Minimum Public Shareholding (“MPS”) for issuers, with the objective of enhancing ease of doing business. The proposed amendments allow large issuers to list with a lower initial public float, providing extended timelines to achieve the required 25% MPS in a gradual manner. The following table captures the recommended transition.

Our View

The bifurcation of post-issue market cap thresholds provides better calibration across different issuer sizes and prevents dilution pressure on large issuers, while simultaneously maintaining investor participation. Further, the revised minimum public offer percentages will ease compliance, ensure significant market float and help sustain liquidity. The timeline extension for MPS compliance will accommodate market absorption capacity and avoid oversupply of shares, which could depress valuations.

(ii) Amendments to the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 with the objective of facilitating ease of doing business and enhancing inclusive participation of institutional investors in the IPO process

Under the earlier framework of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (“ICDR Regulations”), anchor investors were divided into two categories:

• Category I (allocations up to INR 10 crore); and

• Category II (allocations above INR 10 crore and up to INR 250 crore).

SEBI has now approved the proposal to merge the two categories into a single category for allocations up to INR 250 crore.

SEBI has amended the ICDR Regulations to require a minimum of 5 and maximum of 15 investors for allocations upto INR 250 Crore, and for every additional INR 250 crore or part thereof, up to 15 more investors may participate.

Under the extant framework, reservation in anchor book was available only for domestic mutual funds, and under the amended framework, the anchor portion has been increased to 40%, with one-third reserved for domestic mutual funds and the remaining for insurers and pension funds. Further, in case of undersubscription in the reserved portion for Life Insurance Companies and Pension Funds, the unsubscribed part will be available for allocation to domestic Mutual Funds.

Our View

These amendments are expected to broaden anchor investor participation by easing participation for large Foreign Portfolio Investors (“FPIs”) operating multiple funds, thus enabling more diversified anchor books and aligning with global best practices. In addition, it will provide structured and consistent participation opportunities to long-term institutional investors such as life insurers and pension funds, thereby enhancing credibility, stability, and quality of the anchor book.

(iii) Amendments to the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 and the circulars thereunder with the objective of facilitating ease of doing business relating to related party transactions (“RPT”)

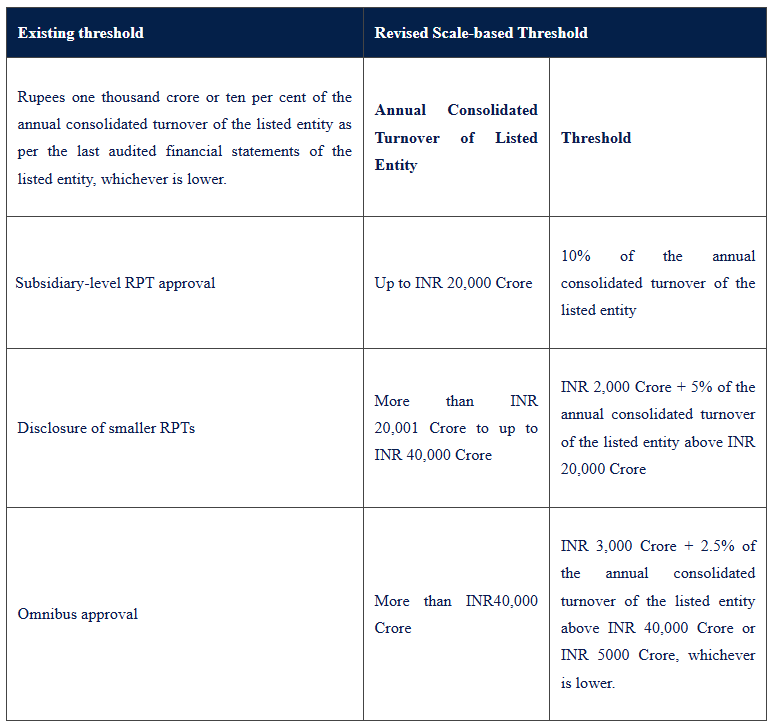

Introduction of scale-based thresholds based on annual consolidated turnover of the listed entity, for determining material RPTs

SEBI has decided to introduce scale-based threshold considering the annual consolidated turnover of the listed entity as per last audited financial statements, for determining material Related Party Transactions (“RPTs”) for approval by shareholders as under:

Revised thresholds for approval by Audit Committee, for RPTs undertaken by subsidiaries

Threshold for prior approval of audit committee of listed entity for RPTs (above rupees one crore), whether entered into individually or taken together with previous transactions during a financial year, undertaken by subsidiaries has been revised in order to remove ambiguity, where RPTs undertaken by subsidiary being classified as material RPT and therefore requires approval of shareholders of the listed entity, but does not require approval of audit committee of the listed entity. The revised threshold for prior approval of audit committee of listed entity are as under:

1. For subsidiary having audited financial statements: ten percent of the annual standalone turnover of the subsidiary as per the last audited financial statements of the subsidiary or the scale-based threshold for material RPT of listed entity, whichever is lower.

2. For subsidiaries not having audited financial statements for a period of at least one year: ten per cent of the aggregate value of paid-up share capital and securities premium account of the subsidiary; or the scale-based threshold for material related party transactions of listed entity, whichever is lower.

SEBI has decided to issue a Circular for specifying minimum information to be provided to the Audit Committee and shareholders for the approval of RPT, which does not exceed 1% of annual consolidated turnover of the listed entity or INR 10 Crore, whichever is lower, whether individually or taken together with previous transactions during a financial year (including transaction(s) which are approved by way of ratification). This will provide relaxation to these RPTs, from the RPT Industry Standards as mentioned in the SEBI Circular dated June 26, 2025.

SEBI has decided that retail purchases from any listed entity or its subsidiary by its directors or key managerial personnel or their relatives, without establishing a business relationship, at the terms which are uniformly applicable/offered to employees as well as abovementioned persons would not be considered “related party transactions”.

Our View:

In our view, the numerical thresholds such as INR 1,000 crore or INR 10 crore are arbitrary and disproportionate. Percentage-based thresholds, tailored to the entity’s financials, would provide a more rational, sector-sensitive test.

Secondly, harmonization of subsidiary-level thresholds with listed entity thresholds is a welcome step, as it addresses regulatory arbitrage, but discretion must remain with audit committees to assess context-specific transactions.

Thirdly, codifying omnibus approval validity periods into regulations enhances clarity, while aligning exemptions for retail purchases and clarifying that “holding company” means only a listed holding company introduces consistency in industry practices and removes existing ambiguities.

(iv) Measures in relation to FPIs

(a) Ease in FPI Registration for IFSC Retail Schemes

SEBI has approved amendments to the SEBI (Foreign Portfolio Investors) Regulations, 2019, to enhance ease of doing business for FPIs in International Financial Services Centres (“IFSCs”). The amendments permit retail schemes in IFSCs with resident Indian sponsors/managers to register as FPIs, align sponsor contribution limits with IFSCA regulations by capping them at 10% of the fund's corpus, and allow overseas Mutual Funds/Unit Trusts registered as FPIs to include Indian mutual funds as constituents, subject to specified conditions, fostering harmonized regulations and increased fund inflows.

Our View:

These amendments significantly contribute to a harmonized functioning between SEBI and the IFSCA, and have the potential to enable significant increases in fund inflows to India. The alignment of sponsor contribution caps with IFSCA creates a more cohesive framework for fund operations across different regulatory jurisdictions within India.

(b) SWAGAT-FI Framework for FPIs and FVCIs

SEBI has approved the introduction of the Single Window Automatic & Generalised Access for Trusted Foreign Investors (“SWAGAT-FI”) framework for FPIs and Foreign Venture Capital Investors (“FVCIs”). Eligible low-risk investors, including government-related entities, sovereign wealth funds, and regulated public retail funds, can opt for SWAGAT-FI status at registration or conversion. Benefits include exemptions from the 66% unlisted asset requirement for FVCIs, 10-year registration validity, exemption from the 50% NRI/OCI contribution cap, and a single demat account option to streamline investments and reduce compliance costs.

(c) Launch of 'India Market Access' Website for FPIs

SEBI, in collaboration with leading Market Infrastructure Institutions ("MIIs"), has launched the 'India Market Access' website as a single-window digital platform. This 360° gateway provides streamlined, consolidated regulatory and procedural information to facilitate seamless FPI entry and ongoing compliance in India's securities markets.

(v) Ease of Doing Business For Accredited Investor-Only Schemes and Relaxations for Large Value Funds

SEBI has approved proposals to introduce Accredited Investor-only (“AI-only”) schemes for accredited investors in Alternative Investment Funds (“AIFs”), exempting them from pari-passu treatment, extending tenure up to 5 years, and removing investor caps. Additionally, Large Value Funds (“LVFs”) are permitted with flexibilities, including exemptions from Private Placement Memorandum requirements and audits, with a reduced minimum investment threshold from INR 70 crore to INR 25 crore, to enhance ease of doing business.

Our View

The introduction of AI-only schemes recognizes the sophisticated nature of accredited investors and provides greater flexibility in fund structuring and management. The reduction in the LVF threshold from INR 70 crore to INR 25 crore significantly expands the potential investor base while maintaining the high-value nature of these investment vehicles.

(vi) Measures relating to REITs and InvITs

(a) Facilitating enhanced participation of Mutual Funds in Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs)

Under the extant framework of SEBI (Mutual Fund) Regulations, 1996, both Real Estate Investment Trusts (“REITs”) and Infrastructure Investment Trusts (“InvITs”) were classified as “hybrid” instruments for the purpose of investments by mutual funds and specialised investment funds. However, now SEBI has decided to classify REITs as “equity” instruments, while InvITs will continue to remain under the “hybrid” classification.

Further, a mutual fund scheme cannot invest more than 10% of its NAV in units of REITs and InvITs, and within this, investment in units of a single issuer is capped at 5% of NAV. However, with REITs now being reclassified as “equity,” investments in REITs will now count towards equity allocation limits, while the entire “hybrid” limit will remain exclusively available for InvITs. Additionally, following reclassification as “equity,” REITs will become eligible for inclusion in equity indices.

Our View

We agree with the classification of REITs as equity, and believe that a similar treatment should be provided in relation to InvITs as well, instead of classifying them as hybrid. Both, REIT and InvIT units are structurally and economically closer to equity. They (i) represent residual ownership; (ii) are publicly traded; (iii) are settled through stock exchanges; and (iv) derive returns from underlying performance, similar to dividends.

The hybrid categorisation is outdated and restrictive, particularly as these instruments have grown in scale and maturity. Further, the re-classification aligns with global practices where REITs are fully integrated into equity markets and indices, thereby unlocking passive fund inflows, enhancing liquidity, and lowering cost of capital. With India’s real estate and infrastructure sectors poised for multi-decade growth, this amendment will expand market depth, improve price discovery, and channel long-term institutional capital into critical asset classes.

(b) Expanding the Scope of "Strategic Investor" for InvITs And REITs to Facilitate Wider Investor Participation

SEBI has approved amendments to expand the “Strategic Investor” definition under the SEBI (Infrastructure Investment Trusts) Regulations, 2014, and SEBI (Real Estate Investment Trusts) Regulations, 2014. The amendment includes all Qualified Institutional Buyers with a minimum corpus of INR25 crores, family trusts and SEBI-registered intermediaries with a net worth exceeding INR500 crores, and various RBI-registered NBFCs as Strategic Investors under the aforesaid regulations, to encourage wider investor participation and enhance utilization of the Strategic Investor Portion in InvIT and REIT public issues.

(vii) Facilitating Enhanced Investor Protection and Financial Inclusion in Mutual Funds

SEBI has approved several proposals to enhance investor protection and promote financial inclusion in the mutual fund industry;

1. Reduction of maximum permissible exit load from 5% to 3%;

2. Revision of incentive structure for distributors for new inflows to mutual fund industry from B-30 cities (Beyond top 30 cities). The incentive would be provided to the distributor for new investors at the industry level and such incentive shall be capped at 1% of the first application amount (in case of lumpsum investment) or total investment during the first year (in case of SIP) subject to a maximum of INR 2000/-.

3. Introduction of an incentive structure for distributors for on-boarding new women investors – Additional commission would be paid to distributors for investment/inflows from new women individual investors (new PAN) at the industry level. The computation and payment of such commission shall be on the same lines as for B-30 incentive

(viii) Measures for Ease Of Doing Business for Entities Having Listed Non-Convertible Securities

SEBI has approved amendments to regulations governing the delivery of annual reports for issuers of listed non-convertible securities. The amendment permits the issuers to send a web-link letter (optionally with a static QR code) instead of hard copies to debenture holders without registered email addresses. Further, timelines will be specified for sending annual reports, aligned with the Companies Act, 2013, or the relevant statute governing the entity, to streamline the compliance requirements.

(ix) Review of Regulatory Framework for Registrars to an Issue and Share Transfer Agents

SEBI has approved amendments to the regulatory framework for Registrars to an Issue and Share Transfer Agents (“RTAs”). The amendments limit SEBI’s regulatory purview to RTA services for listed companies, allowing services to unlisted companies through a Separate Business Unit with a disclaimer, which was not permissible under earlier regulatory framework. Additionally, RTA categorizations (Category I and II) are removed, a common RTA definition is introduced, net-worth requirements and fee structures are revised, and an institutional mechanism is mandated, including senior management oversight, surveillance systems, escalation mechanisms, and a whistleblower policy to enhance governance and fraud prevention.

(x) Proposals for Ease of Doing Business (EoDB) for Investment Advisers and Research Analysts

SEBI has approved amendments to framework for Investment Advisers (“IAs”) and Research Analysts (“RAs”) to promote ease of doing business and enhance operational efficiency. The amendments permit IAs and RAs to share certified past performance data with clients, including prospective ones, in a standardized template certified by an ICAI/ICMAI member, through one-to-one communication for a two-year period following the operationalization of the Past Risk and Return Verification Agency (“PaRRVA”).

Additionally, IAs are now allowed to provide second opinions on assets under pre-distribution arrangements, charging an Asset Under Advice-based fee capped at 2.5% of the asset value per annum, with mandatory disclosure of dual charges (advisory fee and distributor's commission) and annual client consent.

The eligibility criteria for IA/RA registration have been expanded to include graduates from any stream, provided they obtain specified NISM certifications, broadening the talent pool. Furthermore, requirements to submit proof of address, CIBIL reports, net worth/asset liability statements, and infrastructure details have been eliminated, simplifying the registration process significantly.

(xi) Strengthening Governance of Market Infrastructure Institutions (MIIs)

SEBI has approved the following amendments to SEBI (Stock Exchanges and Clearing Corporations) Regulations, 2018, and SEBI (Depositories and Participants) Regulations, 2018;

1. Appointment of Two Executive Directors (“EDs”) to the Governing Board - Mandating the appointment of two EDs, each heading "Vertical 1: Critical Operations" and "Vertical 2: Regulatory, Compliance, Risk Management, and Investor Grievances," as Key Management Personnel (“KMPs”) and will serve on the MII's Governing Board.

2. While the EDs will report to the MD of the MII, the NRC of the Governing Board shall take inputs from the MD and the appropriate committee of the Governing Board in finalizing the appraisal of the EDs.

3. The process of appointment or removal of the EDs will mirror the extant process for the MD.

4. The broad roles and responsibilities of the Managing Director (“MD”), the proposed EDs, and specific KMPs such as the Chief Technology Officer (“CTO”) and Chief Information Security Officer (“CISO”) will be clearly defined.

5. Establishment of clear norms for the directorships of MDs and the proposed EDs of an MII in other companies.

Our View

• Mandating two EDs for Vertical 1 and Vertical 2 risks overlapping roles, administrative redundancies, and governance inefficiencies in MIIs.

• Prescriptive role definitions for MD, EDs, and KMPs (CO, CRO, CTO, CISO) may restrict MIIs’ adaptability and weaken governance by fragmenting roles. In our view, board policies could have been set out in the regulations, thereby allowing MIIs more flexibility in defining roles and responsibilities via board-approved policies.

• A blanket ban on MDs and EDs holding external directorships may deter qualified professionals and limit beneficial sector engagement.

You can mail us your queries and comments at info@finseclaw.com.

DISCLAIMER: The contents of this mail should not be construed as legal opinion. Recipients should take independent legal advice before acting on any views expressed herein.