The Securities and Exchange Board of India (“SEBI”) has issued a consultation paper on August 04, 2025, proposing amendments to the provisions relating to Related Party Transactions (“RPTs”) under SEBI Listing Obligations and Disclosure Requirements Regulations, 2015 and circulars thereunder (“Consultation Paper”).

The Consultation Paper seeks to recalibrate rules for RPTs undertaken by listed entities and their subsidiaries. The proposals reflect recommendations ofSEBI’s Advisory Committee on Listing Obligations and Disclosures and are elaborated below.

PROPOSALS THROUGH THE CONSULTATION PAPER

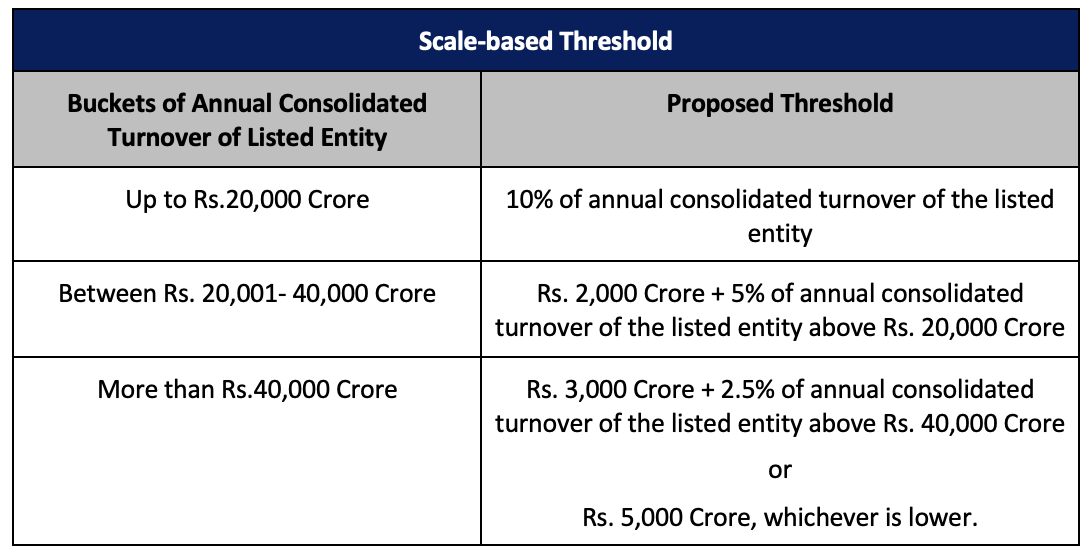

(i) Material RPT Thresholds for listed entities

Currently, Regulation 23(1)of the SEBI Listing Obligations and Disclosure Requirements Regulations,2015 (“LODR”) treats an RPT as material when its value exceeds Rs. 1,000 Crore or ten per cent of a listed entity’s annual consolidated turnover, whichever is lower. This flat benchmark applies regardless of a company’s scale and has been criticised as onerous for high‑turnover entities.

SEBI proposes to amend Regulation 23(1) of LODR by introducing a scale‑based threshold mechanism tied to turnover buckets.

(ii) Material RPT thresholds for subsidiaries of listed entities

Under the current framework, second proviso to Regulation 23(2) of LODR provides that‘a related party transaction to which the subsidiary of a listed entity is a party but the listed entity is not a party, shall require prior approval of the audit committee of the listed entity if the value of such transaction whether entered into individually or taken together with previous transactions during a financial year exceeds ten per cent of the annual consolidated turnover’.

However, it has been observed that, in certain instances, transactions undertaken by the subsidiary may exceed the material RPT threshold requiring shareholder approval yet avoid audit committee scrutiny. To harmonise the regulatory framework, it is proposed that if a subsidiary of a listed company enters into a related party transaction worth more than ₹1 Crore, and the listed company itself is not directly involved, the audit committee of the listed company must give prior approval if the total value of such transactions (alone or combined with earlier ones in the same financial year) exceeds the lower of two thresholds:

a) Ten percent (10%) of the subsidiary’s standalone networth, as per its most recent audited financial statements.

However, if the subsidiary does not have audited financial statements for at least one year then the net worth shall be computed as of a date not more than three months prior to the date of seeking audit committee approval. Furthermore, if the subsidiary has a negative net worth, it shall be substituted with the aggregate value of the subsidiary’s paid-up share capital and securities premium, also computed as of a date not more than three months before the date of seeking approval.

b) Threshold for material RPT of listed entity as determined in accordance with Schedule XII under Regulation 23(1) of LODR.

Aligning thresholds in this manner ensures that significant subsidiary transactions receive both audit committee and shareholder scrutiny.

(iii) Validity periods for shareholder omnibus approvals

The Consultation Paper also proposes to codify validity periods for shareholder omnibus approvals. The proposal seeks to amend Regulation 23(4) of the LODR to provide that omnibus approvals granted at an AGM remain valid until the next AGM or for 15 months, while those granted at other general meetings lapse after one year.

(iv) Relaxation in information for audit committee and shareholders

Through its circular dated June 26, 2025, SEBI prescribed Industry Standards for minimum information to be provided to the Audit Committee and Shareholders for approval for RPTs (“RPT Industry Standards”). However, RPT Industry Standards do not apply to transactions below Rs. 1 Crore with a related party to be entered into individually or taken together with previous transactions during a financial year (including which are approved by way of ratification).

Industry bodies have argued that this threshold is minuscule for large companies. The ConsultationPaper proposes that for RPTs between Rs. 1 Crore and, lower of (1% consolidated turnover or Rs. 10 Crores), the company may furnish a simplified disclosure, as outlined in the proposed draft circular titled Industry Standards on “Minimum information to be provided to the Audit Committee and Shareholders for approval of Related Party Transactions”. Additionally, transactions beyond the 1% or Rs. 10 Crore thresholds would continue to attract the comprehensive RPT Disclosure Standards.

(v) Clarifications on applicability of RPT provisions

Through the Consultation Paper, SEBI has also sought to clarify the applicability of certain provisions relating to RPTs under the LODR. Firstly, retail purchases made by directors or employees from a listed entity or its subsidiary are not considered RPTs, provided such purchases do not establish a business relationship and are made on terms uniformly applicable to all employees and directors. It is proposed that proviso (e) to Regulation 2(1)(zc) of the LODR Regulations be amended to extend the exemption to directors, key managerial personnel of the listed entity or its subsidiary, and their relatives.

Secondly, clause (b) of Regulation 23(5) of the LODR exempts transactions between a holding company and its wholly owned subsidiary from the applicability of sub-regulations (2), (3), and (4) of Regulation 23. In this regard, SEBI received representations seeking clarity on whether the clause applies to listed holding companies or unlisted holding companies as well. SEBI now proposes to insert an explanation in the regulations to clarify that the term ‘holding company’ refers to, and shall be deemed to have always referred to, a listed holding company.

CONCLUSION

SEBI’s proposals seek to recalibrate materiality thresholds, streamline disclosure sand clarify exemptions for RPTs. By tying the materiality test to turnover, aligning subsidiary thresholds, codifying the validity of omnibus approvals and tailoring disclosure requirements, the proposals aim to facilitate ease of doing business while preserving safeguards for minority investors. Stakeholders have until August 25, 2025, to provide feedback on these proposals.

You can mail us your queries and comments at Manas Dhagat and Purva Mandale.